The state of digitalisation in the banking and insurance sectors

Nov 02, 2020

INTRODUCTION

The advent of digitalisation is changing the environment of financial institutions (retail banking and life and non-life insurance companies) around the world, in terms of the skills profile of employees and the organisation of teams from front to back office. It is also an increasingly used trading channel in many developing countries, particularly sub-Saharan Africa, and has many comparative advantages for both consumers and financial institutions in terms of accessibility and transaction costs.

The number of financial institutions’ agencies and customer reception points will likely decline in the coming years, with customers performing certain operations remotely or on automatic and “smart” machines. This transformation should spur financial institutions to devote their reception points and sales agencies to focus on their core business, i.e. advice and expertise (real estate projects, savings plans, life insurance, health coverage, etc.). The transition to digital technology will also enhance the quality of service to customers, who in turn will have remote and easy access to personalized products and services. The digitalisation of financial services is also accelerated by mobile telephony, which in sub-Saharan Africa has a mobile penetration rate of 43% according to the Global System for Mobile Communications (GSMA). East Africa began its digital transformation a few years ago, including Kenya, through M-Pesa: a mobile financial services tool, or mobile money, that has captured the potential of digital services and optimised their use and accessibility to the local population. These changes in consumption habits and transaction patterns imply regulatory adaptation measures for the management of digital financial services, in order to enhance their quality but also to enhance customer confidence in the risks inherent in the technology; these include potential fraud, false transactions and consumer privacy protection.

In the face of the health and economic crisis caused by the COVID-19 pandemic, digitalisation is also proving to be a justified and efficient transition for institutions providing financial services insofar as it de facto reduces the health risks inherent in the spread of the pandemic, and above all makes it possible to maintain the provision of financial services to customers by reducing in the medium and long term the transaction costs associated with services in agencies and reception points of banking networks. Thus, this health crisis represents an opportunity for banks and other financial institutions to develop their digital terminal networks in order to optimise their customer service provision. As a result, the rise in digitalisation, coupled with the reduction in consumer mobility caused by the health crisis, is enabling African banking and financial institutions to limit their potential financial losses in this global economic downturn and, above all, to build a new paradigm in their approaches to customer relations.

BACKGROUND AND ANALYSIS

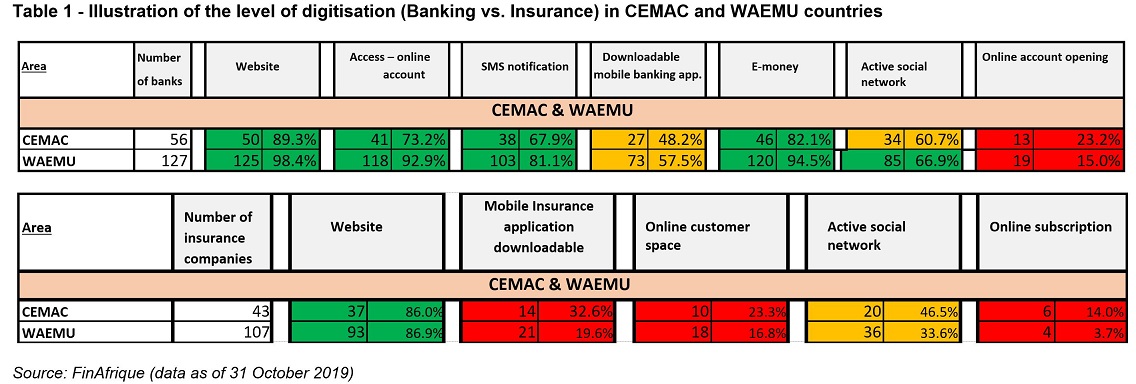

FinAfrique conducted a study (data as at 31/10/2019) on "the situation of digitalisation of customer services in Banking and Insurance in 21 sub-Saharan African countries". This study sought to assess the disparity in the level of digitisation of remote customer services, in particular via Internet sites, mobile phones, social networks and the possibility of having remote access to one’s bank account or to information relating to one’s contract. This study also helped to contrast these outcomes in two monetary zones in West Africa (WAEMU) and Central Africa (CEMAC).

Out of the 21 countries studied, the higher penetration rate (18% in the banking sector compared to about 1.4% in the insurance sector) in the banking sector compared to the insurance sector strongly explains the disparities recorded in the level of digitisation under all the areas analysed (presence on the Internet, possibility of buying products online or consulting information on contracts, etc.).

Moreover, in all 21 countries studied, banking sector customers are better connected and can easily access either information about their contracts and services (via sms or mobile applications) or information about their institutions (via social networks or websites) compared to insurance companies’ customers. These digital financial services include, among others, automated teller machine (ATM), card and contactless payment services, online and mobile applications using the Internet, and mobile money-based payment methods (USSD system).

From a geographical point of view, the banking sector of the WAEMU area appears significantly better connected than that of its neighbour CEMAC, with 98.4% of establishments equipped with an Internet site in the WAEMU area compared to 89.3% in the CEMAC area, and just over one in two banks (57.5%) in the WAEMU area offers a mobile application, compared to 48.2% in their Central African counterparts. In comparative terms, East Africa remains slightly ahead of the two above-mentioned regions in terms of access to remote banking and financial services. According to the PriceWaterhouseCoopers (PwC) report , “ East Africa Banking Survey 2019 ,” 66% of banking institutions in the East African region offer online and mobile money banking services, and 61% of customer transactions are digital. Thus, based on the fact that East Africa is the most dynamic region on the continent in terms of digital and mobile payments, it can be seen that the West and Central African regions perform rather similarly to East Africa even though, compared to East Africa, they lag slightly behind in terms of penetration of digital financial services.

Also, although there is a certain deficit of online account opening services on most of the banks' mobile applications in the two study areas, it should be noted that online account management services as well as services allowing transactions to be carried out through the digital channel are well available in both sub-regions. Beyond the existence of digital platforms in most credit institutions, online account opening services (CEMAC 23.2%, WAEMU 15.0%) are far less available than online account access services (CEMAC 89.3%, WAEMU 98.4%).

At the level of regulatory frameworks, the provisions governing the digitisation of financial services to customers have almost different approaches. In CEMAC, Regulation No. 4/18/CEMAC/UMAC/COBAC reinforces the focus on the management of payment services to financial institutions under the supervision of the sectoral regulator, and of their distribution networks. In contrast, WAEMU, through Instruction No. 008_5_2015, is moving towards popularising the digitisation of financial services through electronic money, which includes a greater number of platforms and players in the management of the digitisation of financial services.

In the insurance sector, the proportions are reversed in favour of the CEMAC area, although in absolute terms, there are more insurance companies digitised in WAEMU. Thus, 46.5% of the insurance companies in the CEMAC zone - i.e. 20 out of a total of 43 - are active on social networks, compared to 33.6% in the WAEMU area - i.e. 36 out of the 107 companies in this sub-region. Despite the relative presence of insurance companies on the web interface, there is a certain deficit in terms of accessibility and underwriting of insurance services via existing digital channels. In fact, online subscription rates in CEMAC and WAEMU areas are low and stand at 14% and 3.7% respectively.

In summary, this study found that the vast majority of African financial institutions (banks and insurance companies) have at least one website as a showcase and commercial interface, even if efforts still need to be made in some countries, including the Central African Republic, to stimulate the use of digital channels in financial services. However, in the vast majority of the countries surveyed, consumers have very little opportunity to open a bank account online or to take out an insurance policy remotely. Gabonese banks are the model for all the countries studied, with 42.9% of them already implementing these online services for their customers. It should also be noted that Chad (22.2%), the Central African Republic (16.7%), Burundi (27.3%) and Mauritania (33.3%) are the countries for which banking customers are the least well off on the African continent in terms of mobile applications to access their accounts and banking services. A large number of financial institutions in the CEMAC (82.1%) and WAEMU (94.5%) areas provide their customers with means of payment, but only 50% of Central African bankers facilitate this service compared to 100% in Cameroon and Côte d'Ivoire for example. Across all the countries studied, Côte d’Ivoire appears to be the country with the highest penetration of digital banking services: either through a web-based client space offered by 100% of the country’s 26 credit institutions, or by a downloadable mobile application (69.2% of credit institutions). As for the insurance sector, Cameroon stands out in the two sub-regions with 9 out of 22 companies offering their clients an online customer space and a mobile application.

CONCLUSION

The main challenges facing financial institutions operating in the 21 countries analysed are the deployment of reliable information systems, including the choice of appropriate technology, the quality of collaboration between different financial institutions’ services without increasing tariffs for consumers. The low cost of the investments required to ensure visibility on social networks, widely frequented by potential youth clientele, certainly explains the rapid development of the activity of financial institutions on these communication channels; compared to the reaction of local financial institutions to Internet marketing strategies some 20 years ago.

The major changes inherent in socio-cultural developments, the organisational structure of financial institutions, and the support of different regulators, will move all financial sector actors hitch-free into the digital world. To this end, companies must inform and train all their employees so that the transition is effective in the ways of thinking and in the internal workings of these organisations. Clearly, business changes in the financial sector will necessarily take place through three strategic steps, which are as follows:

- First, the extension of basic financial services to a larger number of beneficiaries through the strengthening of financial education policies, the adaptation by financial institutions of their products and services to semi-urban, rural and low-income customers.

- Second, domestic and sub-regional financial sector actors will need to strive to facilitate and intensify domestic and cross-border transactions by establishing interoperable platforms for linking bank accounts, online, card, or mobile money payment solutions. accounts in microfinance institutions and insurance or micro-insurance products.

- Finally, the maturation phase of the financial sector should correspond to an effective integration of artificial intelligence and robotics tools that will enable a personalized and proactive response to customer needs while improving the services and products of financial institutions. As a result, business process automation, customer data analysis, and control will significantly save time and boost productivity.

Ultimately, the digitalisation of financial services in both regions will likely foster the concentration of domestic financial sectors and provide financial institutions with the volumes of assets needed to respond effectively and sustainably to the ever-increasing needs of clients. These financial institutions should take advantage of the increase in the rate of mobile and smartphone usage among the population to improve the customer experience and thus increase the sales of their products tenfold, and thus their profitability thanks to digitisation.

About the author

Léticia Ngahane Konan is Associate Director in charge of West Africa for the advisory firm FinAfrique. She manages missions related to digital and actuarial techniques in bancassurance in Sub-Saharan Africa. She previously worked for 9 years as an actuary in banks and insurance companies in France and Luxembourg, focused primarily on issues related to profitability, reinsurance and Solvency I & II regulations. Passionate about IT, over the course of her career she has developed numerous actuarial tools that have made it possible to optimize financial and actuarial processes in the bancassurance sector in Europe and Africa. She graduated from the University of Grenoble and Strasbourg and is a member of the Institute of Actuaries (France).

Your comment