Public Development Banks and Social Housing in Africa

Nov 05, 2024

Introduction

The mobilization of public resources remains a major problem in Africa. Most African countries have limited fiscal space, due to a narrow and poorly diversified tax base. Solutions to this problem remain hypothetical in a context characterized by repeated exogenous shocks, notably climate change with its effects on the volatility of agricultural production and commodity prices. Additionally, harmful security environments and persistent political instabilities in several African countries keep the implementation of public resource mobilization policies relatively sluggish. These constraints appear to be more burdensome given the long-term financing needs required for the implementation of the National Development Plans (NDPs), of which access to social housing remains an absolute priority. Using a comparative approach, we present the asset structure of the public development banks[1] (PDBs), while highlighting the importance of PDBs in the social housing sector.

What is the asset structure of PDBs?

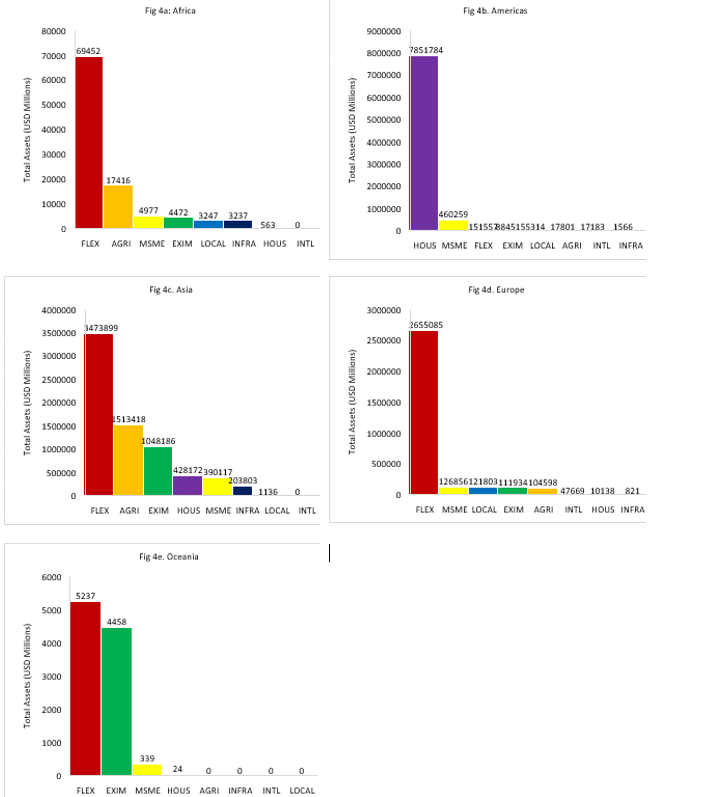

Overall, PDBs whose official mandate relates to general development (FLEX[2]) hold the majority of assets in most regions, except for America where PBDs whose official mandate is assigned to social housing hold 7,851,784 million USD of assets, which represent nearly 91% of the total (Figure 1).

Figure 1. Structure of BPD assets

Source: Public Development Banks (PDB) and Development Financing Institutions (DFI) Database (Peking University, Institute of New Structural Economics, last update: January 2024)

Note: General Development (FLEX), Small and Medium-Sized Enterprises (SMSE), Promoting Export and Foreign Trade (EXIM), Rural and Agricultural Development (AGRI), International Financing of Private Sector Development (INTL), Social Housing (HOUS), Infrastructure (INFRA) and Local Government (LOCAL).

What is the importance of PBDs in the social housing sector in Africa compared to America?

It appears from previous analyses that the social housing sector remains marginal in Africa with USD 563 million in assets, representing barely 1% of the total assets of PBDs, compared to more than 90% for American PDBs (Figure 1). The scope of PDBs in financing social housing remains limited in Africa, contrasting by far with the reality in America.

How can we explain the divergence in the importance of African and American BPD on social housing?

The “Great Depression” following the collapse of the US stock market, and the resulting mortgage crisis, led to the creation of 2 major institutions, Fannie Mae[3] in 1938 and Freddie Mac[4] in 1970, two mixed-capital companies with private capital and a public service mission. Fannie Mae and Freddie Mac, through securitization techniques, repurchased mortgage loans from private banks and sold them onto the capital market, thus reducing liquidity risk on the mortgage market. These initiatives led to higher mortgage loan-to-value ratios[5], longer maturities (20 to 30 years), and a significant drop in security rates, increasing the number of affordable mortgage loans[6]. Fannie Mae and Freddie Mac provide the bulk of American real estate financing. In 2023, these institutions accounted for approximately half of the US’ outstanding residential mortgage debt.

Between the 1960s and 1970s, the majority of African countries, at the dawn of their independence, were still characterized by a low rate of urbanization with only 15% of Africans living in cities in 1950,[7] and limited resources and institutional capacity that could support the implementation of large-scale housing programs. Government projects aimed at addressing the needs of low-income households remained marginal and often interrupted in their implementation, due to political instabilities. Until the 1990s, the supply of social housing in African countries represented less than 5% of total housing production[8]. This fact, which did not exempt some relatively prosperous countries at that time such as Ivory Coast [9] and Nigeria[10], highlighted a real lack of political will and an absence of government leadership in formulating adequate policies, key to responding to the growing affordable housing concern. In addition, the systemic crises in sub-Saharan Africa’s banking sector from the 1970s in English-speaking countries and 1980s in French-speaking Africa, which originated from fragilities[11] linked to development banks, resulted in major consequences: the broadening of PDBs’ activities to that of commercial banks, which progressively phased out of specificities inherent to their former mandates. However, supranational development banks, which were relatively less impacted by this crisis than their national counterparts, continued to play a key role throughout the continent[12].

The phasing out of the specificities assigned to PDBs’ mandates, notably those in the housing sector, also favored the rapid changes that occurred in African financial systems. These include the rise in power of private commercial banks with their growing mortgage loan, the stepping in of new technical and financial partners such as the International Finance Corporation (IFC), the setting of Public-Private Partnerships (PPP), and other alternatives including presidential social housing programs such as those initiated in Ivory Coast[13]. Moreover, there is a growing dynamism of decentralized microfinance institutions and other innovations at the sub-regional level such as the Regional Mortgage Refinancing Fund of the West African Economic and Monetary Union[14] (CRRH-UEMOA) whose mission is to offer long-term resources for the refinancing of mortgage loans granted by WAEMU credit institutions to their clients. CRRH-UEMOA generates funds either by issuing bonds on the regional financial market or by mobilizing concessional resources[15].

Conclusion and Recommendations

The reconfiguration of the financial landscape since the outbreak of the banking sector systemic crises that occurred in the 1970s and 1980s in Africa has led to a significant reduction in PDBs dedicated to sectoral financing of the economy, and a rise in the power of private commercial banks, in a rapidly changing financial environment caused by digital finance.

Although PDBs have played an essential role in deepening national financing systems, the era of sectoral PDBs, particularly in the housing sector, now seems almost over.

However, the successful implementation of new alternative mechanisms for financing social housing requires a set of conditions to be met.

The exploration and adoption of innovative and sustainable partnership models between governments, private sectors, and technical and financial partners, either bilateral and multilateral entities or at the regional or international level, should not only be intensified but most importantly adapt practically to the socio-economic environment of African countries. Such a context requires the re-examination of the regulatory and institutional framework, and a redefinition of respective roles, particularly those belonging to the state whose fiscal sustainability needs require an optimal use of public subsidies.

Combined collaborative efforts between the public and private sectors appear to give “public-private” partnerships greater adaptability to macroeconomic changes, thereby contributing to strengthening the counter cyclicality of financing systems.

The comparative advantages offered by CRRH-UEMOA through its capacity to raise long-term resources and attractive rates should be leveraged by WAEMU States by implementing policies aimed at promoting greater financial inclusion.

The narrowness of the capital market in the WAEMU could constitute an obstacle to the sustainability of the CRRH-UEMOA’s impact. This implies the strengthening of policies promoting a deeper capital market, broader investor base, and greater diversification of financial products offered.

Finally, reforms allowing easier acquisition of land deeds, which are required as collaterals, should also be implemented to promote mortgage loans in the housing sector.

[1] Public Development Banks and Development Financing Institutions Database (PEKING UNIVERSITY, Institute of New Structural Economics). http://www.dfidatabase.pku.edu.cn/DataVisualization/index.htm# (last updated: January 2024)

[2] FLEX is referred to as GENERAL DEVELOPMENT, according to PDBs’ official mandate.

[3] Originally known as « Federal National Mortgage Association »

[4] Originally known as « Federal Home Loan Mortgage Corporation »

[5] Snowden, K. (2014). Mortgage banking in the United States, 1870–1940. September 10, 2014. Research Institute for Housing America Special Report.

[6] Leicht, A. (2022). History of the American mortgage. January 7, 2022. Better. https://better.com/content/history-of-the-american-mortgage.

[7] UN-Habitat (2011). Affordable land and housing in Africa. Volume 3. Pg. 5.

[8] UN-Habitat (2011). Affordable land and housing in Africa. Volume 3.

[9] In Ivory Coast, the world's leading cocoa producer, social housing represented only 2,000 homes per year between 1960 and 1983.

[10] In oil-rich Nigeria, the construction of 202,000 housing units was proposed for the period 1975-1980 (40,000 per year), but only 28,500 units in total were built during this period.

[11] Mixed results of projects weakening the profitability of banks and the maintenance of their capital, poor or fraudulent management of managers, ineffectiveness of strategies, etc.

[12] See note 17. Pg. 8.

[13] It is known as the Presidential Social and Economic Housing Construction Program (PPCLSE). Outside of UEMOA, Cameroon and Chad have also initiated presidential social housing programs.

[14] Created in 2010 and became operational in 2012, with a share capital amounting to just over 10 billion CFA (16.6 million US$) at the end of 2021. It includes 58 shareholder banks, or approximately two thirds of the bank commercial companies in the community space holding two thirds of the capital. The remaining third is shared between BOAD, the International Finance Corporation (IFC), the Investment and Development Bank of the Economic Community of West African States (EBID), and Shelter Afrique. The various mechanisms that CRRH-UEMOA uses include refinancing, securitization and guarantee.

[15] Interview with Ms. Yedau Ogoundele, Director General of the WAEMU Regional Mortgage Refinancing Company. The World Bank. https://www.banquemondiale.org/fr/news/feature/2023/11/07/interview-with-yedau-ogoundele-director-general-of-the-waemu-regional-mortgage-refinancing-company. November 7 2023.

Your comment