How fostering digital financial inclusion and bank competition can reinforce financial stability

Jun 27, 2024

Digital financial services have for over two decades grown exponentially thereby driving financial inclusion for billions of people (digital financial inclusion), opening up spectacular opportunities for small businesses and enterpreneurs acrosss the world. The 2024 GSMA report reveals that 15 of the 17 Sustainable Development Goals (SGDs) can be reached when digital financial inclusion is effectively executed (GSMA, 20241). In that regard, the concept of digital financial inclusion has become the catchphrase for researchers, policymakers, and other stakeholders. Given its implications for boosting shared prosperity, it has particularly been highlighted and gained impetus in the topical global policy discussions. Several development agencies have also taken key steps to promote digital financial inclusion, given the important role it plays in the development and the state of economic development in emerging economies.

There is growing evidence that the competitiveness between banks and the degree of inclusivity of a financial system both affect its stability2, 3, 4 &5. Bank competition is of particular interest due to its financial stability implications which affects the economy at large. A study by Chinoda & kapingura (2023) reveals that digital financial inclusion has a significant positive effect on bank stability and a negative effect on non performing loans. The study also found a significant negative effect of bank competition on financial stability. This was in line other studies by Chinoda & Kwenda (2019) and Saha &Duta (2021). Since economies are still recovering from the effects of the COVID-19 pandemic which posed greater risk for the market participants and the financial sector, it’s understandable to focus on the stability of global and national financial systems.

However, policymakers have elevated digital financial inclusion as a fundamental policy goal, alongside financial stability, protection, and integrity. Inclusive economic growth and financial development must balance bank competition, financial inclusion, and financial stability since prioritizing only one component would stifle the others. The banking industry is undergoing change globally, and banks—especially those in developing countries—face intense competition from international institutions. Compared to developed economies, these countries have a greater proportion of unbanked citizens. In an effort to boost financial inclusion and lower the number of unbanked people, banks in emerging economies are turning to digital financial services. This was found to be consistent with our paper on the impact of digital financial inclusion and bank competition on financial stability in Sub-Saharan Africa(see footnote 2). Understanding the link between bank competition, financial inclusion and bank stability is important because where there is uncontrolled competition, market misconduct by banks may negatively impact the financial inclusion and bank stability goals in the region.

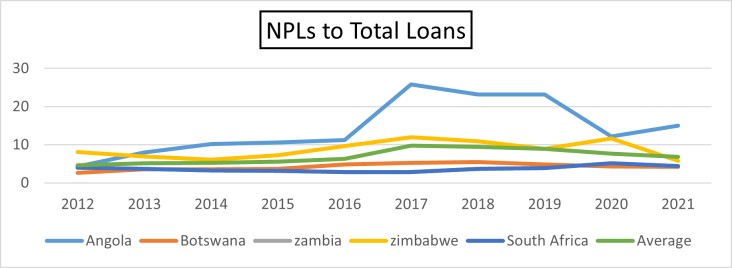

Digital financial inclusion in Sub-Saharan Africa has increased over the last decade. The GSMA 2024 report revealed that there were approximately 435 million active mobile money accounts by the end of 2023-an annual increase of 9%, compared to 13% and 15% in 2022 and 2021 respectively. The COVID-19 epidemic caused these activities to pick up speed. Mobile money-driven activities increased along with the digital economy, leading to notable developments in some Sub-Saharan African nations, including Zimbabwe (Ecocash), Kenya (M-Pesa), South Africa (E-wallet). West Africa has however emerged as a key player in the past decade with the number of registered mobile money accounts doubling between 2013 and 2023 mostly driven by growth in Ghana, Senegal and Nigeria (GSMA, 2024. Many users of mobile money are now capable of accessing productive services that were previously inaccessible. However, at the same time, bank stability in the SSA region seems to have been threatened over the period 2012 to 2017 as witnessed by an increase in average level of non-performing loans for Zimbabwe, Zambia, South Africa, Angola and Botswana from 4.63% to 9.76% before declining to 6.79% in 2021 as shown in Figure 1 below. The growth in the value of mobile money transactions has a tendency to reduce liquidity and capital adequacy ratios of banks and increase non performing loans ratio to total loans. The rise in non-performing loans can hamper banks’ ability to increase financial intermediation. High and rising levels of non-performing loans can put a strain on bank balance sheets, limiting banks’ ability to increase financial intermediation and thus stability. Extensive use of digital financial services is associated with dangers of digital risks such as payment system disruption and data theft which has an adverse effect on financial stability.

However, digital financial inclusion and better bank competition can seperately have a positive impact on financial stability. The results of our study reveal that digital financial inclusion and bank competition accelerate banking stability, which not only reduces bank default risk but also increases opportunities and wealth that can drive social change for families and individual over time (financial mobility)2. (see footnote 2). The provision of basic financial services to both small businesses and disadvantaged populations at an affordable cost in a transparent and fair manner has become a global challenge. In that sense, the growth of digital financial services increases the proportion of the population who utilize formal banking, which reduces market risk, and promote financial sector stability. Digital finance should be implemented inorder for the banking industry to keep up with the competitive world and ensure sustainable economic development and banking stability. The competition pattern of banking is reshaped by the development of digital finance, which has a positive effect on bank competition. Digital finance promises to enhance gross domestic product of economies which are digitalised by providing convinient access to diverse range of financial services and products for individuals and small to large businesses, which can consequently lead to financial stability. Digital finance also lead to increased financial intermediation and economic stability which has a positive effect on financial stability. Digital finance also promises to lower bank costs by reducing queuing lines in banking halls, reduce manual documentation and paperwork, thus leading to efficiency which enhances financial stability.

Digital finance promotes bank competition by improving the inclusiveness of financial services, which expands the scope of service (scale effect). In addition, digital finance promotes competition by improving the risk identification ability, pricing ability and the capital allocation ability (pricing effect). Bank competition reduces monopoly among banks resulting in enhanced financial stability.

However, this requires a certain amount of synergy and trade-offs. Indeed, bank competition and the expansion of access to credit pose risks for both financial services providers and customers in the absence of strong supervision. Certain policies associated with competition and digital financial inclusion efforts, such as credit quotas and interest rate caps, also can have destabilizing effects in some contexts. This can happen when policies distort incentives for lenders and borrowers, thereby reducing asset quality or disincentivizing new banks to enter the market.

Innovations that advance financial inclusion also can pose new risks such as concentration risks, cyber risks, macro-financial risks, market risks and data privacy risks, thus affecting financial stability. However, strong supervision and regulation plays a pivotal role in maintaining financial stability through mitigating the negative impact of fintech. There could be several reasons for countries to experience a high level of financial stability after the induction of regulation. First, regulation offers a tightened environment for experimentation and innovation which allows fintech firms not to engage in riskier activities without sufficient safeguards. The reduced risk-taking can lead to lower default rates, and ultimately enhance financial stability. Finally, regulation reduces concerns among consumers regarding the reliability and stability of financial services. In the presence of effective supervision and regulation, consumer trust is enhanced which can result in a potential increase in deposits. A boost in consumer confidence can enhance financial stability.

On the other side, measures designed to safeguard digital financial inclusion include continued expansion of digital financial services, liquidity support for financial institutions that target unserved and underserved customers, and a customer due diligence risk-based approach. These measures also promote financial stability by contributing to the judicious functioning and diversification of financial institutions. If there are more people who believe and use financial services, this will have positive effects in terms of financial stability because of risk sharing.

Figure 1: Non-Performing Loans in SSA

Source: GFDI Database, World Bank,(2024)

Specifically, policymakers and regulators can apply policies and regulatory enablers of digital financial inclusion, loosen constraints to financial inclusion with stability factors in mind, and push forward on the digital front while keeping an eye on the risks and opportunities of bank competition and fintech. We also call for strategic measures to preserve bank stability, such as complementing digital financial inclusion with financial literacy and enhancing bank competition.

The stakes are high. Digital Financial inclusion needs to remain high on the policy agenda. Policymakers and international bodies should consider the state of bank competition and digital financial inclusion in each country and adapt measures accordingly. Last but not least, digital financial inclusion and monitored bank competition need to be a component of a more inclusive economic recovery especially post-Covid-19.

___________________________________

Your comment