Fintech for SME Lending in Africa

Mar 04, 2024

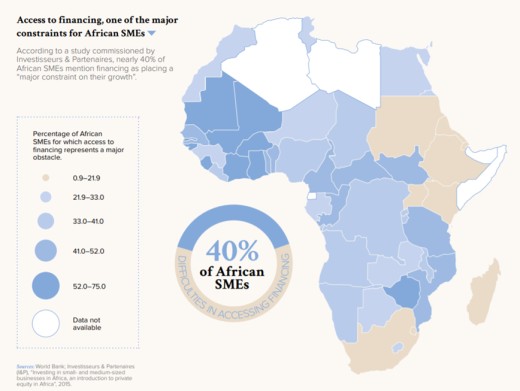

SMEs are the backbone of African economies, providing over 60% of employment, generating some 40% of the GDP. SMEs are merchants, traders, producers, innovators, plumbers, smallholder farmers, hairdressers, restaurants. Some 60 million are registered businesses and probably the same number scrape by as unregistered, often micro-scale, ventures. They need finance for working capital or investments. More than USD 300 billion by some estimates, and in sub-Saharan Africa alone the gap is a massive USD 245 billion according to World Bank numbers. Some 40% of African SMEs have difficulty accessing finance.

SMEs: the “missing middle”

Why? Making loans to them is cumbersome - KYC (know your customer) due diligence and credit assessments are time consuming and therefore costly. Data is often not easily available, corporate governance may be lacking. Most SMEs only need smallish loans, so the potential profits from making such loans are also small. For banks, including development banks, these processes were simply too expensive in the past, so they preferred to focus on bigger corporates, which is understandable. And microfinance institutions lent to individuals and micro enterprises. As a result, SMEs fell between the chairs. The problem of this “Missing Middle” was recognized years ago, alas not much could be done to help these SMEs as long as lending was a tiresome manual or analogue process.

Fintech and digitalization: is this really enough to reduce the financing gap for SMEs?

Then about ten years ago came fintech and started disrupting traditional banking by providing faster and cheaper loans and services to consumers and companies around the world. Digitalization seemed the answer to solve the problem of expensive analogue processes and looked like being the answer to help close the African USD 300 billion gap. Many thought, banks were toast.

Well, things did not happen quite as predicted and the conclusion from analyzing both banks and fintech companies in various countries of the continent is that technology nonetheless seems able to contribute to the expansion of SME lending, even if not in the disruptive way people originally expected.

Let’s look at the basics: If the assumption is that in principle there is enough money available to close the financing gap, then the simple conclusion must be that money does not reach its targets because of red tape, wrong risk-return characteristics or both. Removing red tape is a larger issue. But if the returns were sustainably high enough to compensate for risks, money should flow. How do you increase returns? Not by simply charging more, but by building better processes that reduce the costs of making loans. And by better analyzing and quantifying risks. Fintech, i.e. digitalization, addresses both these issues.

Making loans is expensive for banks. Onboarding a new client requires KYC processes when issues like company registration, fraud registers, directors, major shareholders, ESG standards are checked. Credit assessments are even more onerous, taking between four to six week and in the past even up to six months. Basically the same amount of data-points need to be analyzed for a loan of USD 100k as for a loan of USD 1 million. Spreading such costs over a 100k SME loan would result in a high margin – i.e. the interest rate charged - to an extent that the loan is no longer affordable for an SME, or legal in a country such as South Africa. So if the overheads and costs of KYC and credit assessment can be reduced and if the risk assessment methodology can be improved, lenders can charge sustainable interest rates and still make profits.

So fintechs which promise all of this should have replaced banks by now. Alas, banks still remain the classical SME lenders and loan-volumes from banks for SMEs by far exceed volumes lent by fintech companies. And that despite the fact that the lending processes of banks are in most cases still very traditional, i.e. manual, from on-boarding, KYC, to credit analysis and disbursement processing.

Some banks, however, have realised the advantages digitalization entails and have gone from manual to digital, i.e. internalizing fintech. From the analysis of a number of banks across the continent the following conclusions can be drawn:

- Many banks stick to legacy processes and making SME loans would continue to be expensive for them so that lending may not be expanded.

- But others are waking up and are digitalizing KYC and credit assessment, thus sharply reducing processing times, whilst improving analytics and thus reducing unexpected loan losses.

- One Ruanda-based bank reported time-savings of over 70 hours per SME credit assessment - a conservative indication of the total time saving potential per client in other banks.

- Banks have one big advantage: as deposit taking institutions they generally have a huge domestic funding base that can provide cheap funding for the expansion of SME lending.

- The other advantage of banks is their bricks-and-mortar presence in many parts of the country, which helps keeping the number of non-performing loans in check and is useful in case of loan restructurings and recovery.

Fintech has not always met expectations in terms of costs

Now, let’s look at fintech companies, why have they not pushed banks aside? In some way the oldest fintech in Africa is mobile money. With the spreading of mobile phones, many people and thus also microbusinesses got connected to each other and also to a potential new source of money: cashless money through the phone. M-Pesa, the pioneer in Kenya, brought financial inclusion to literally anybody in the country who was in possession of a simple mobile phone – not even a smartphone. Truly revolutionary at a time when in the UK people were still using checks to make payments, the technology should have disrupted and replaced traditional bank lending. Alas, even more than 20 years later, the money lent through the various mobile service providers in Kenya was a rather small amount of USD 151 million equivalent, totally dwarfed by the USD 5.3 billion equivalent which banks lent to SMEs. Even microfinance institutions lent double that amount. How come? Well, the interest rates charged by mobile money lenders are high, with Safaricom quoting a 9% loan fee for a one month repayment loan which equates to an annualized rate of 181%. Which business can sustain such rates? Sadly, whilst mobile money was truly revolutionary, it failed to disrupt the SME lending market and close the financing gap.

So, where will the disruption come from? There are a number of Peer to Peer (P2P) platforms in Africa connecting SME borrowers with lenders and there are platforms and companies lending directly to SMEs based on decision engines and processes driven by fintech. These lenders and platforms share some characteristics of classical disrupters: they are faster than banks, have no legacy systems or legacy processes and can therefore introduce modern digitalized, AI-supported, KYC and credit processes, thereby greatly reducing the fixed costs per loan made, thus operating at a fraction of the cost of bricks and mortar banks. Their potential lending rates should be every banker’s nightmare. Alas. In reality fintech loans are surprisingly expensive, even if not as bad as mobile money loans. Interest rates of 50 plus% Annual Percentage Rate (APR) or higher may be manageable as a one-off, but cannot become the base for proper working capital finance, let alone for longer term loans to purchase equipment. High lending rates lead to questions of sustainability and runs contrary to the concept of ‘disruption’.

There are several reasons for such high rates. One is the issue that the algorithms developed by fintech companies for credit-scoring have not been tested over enough credit cycles. Yes, Covid provided a highly stressful economic situation with shocks to the demand and supply sides as well as to the supply of financing available so the AI elements (if there are any) of the algorithms should have learned fast. Secondly, the fact that most digital credit analysis focuses on only 3 or 6 months of data, like bank statements, may not lead to the full picture of the creditworthiness of the SME’s business. And then, a major road block: funding. Fintechs generally do not have access to deposits and so funding becomes expensive. Despite initial excitement, impact investors and DFIs are likely, in the medium term, to shun fintech lenders that charge usury rates. But without funding, fintech lenders will not be able to grow their lending business. This leads to a catch-22 situation where fintech lenders may need to charge high interest rates in order to cover potential loan losses due to imprecise credit assessments and as long as this is the case, they are likely to struggle finding credit-funding themselves and therefore cannot significantly expand their lending operations. Only very few start-up lenders decided therefore to go the long route and apply for a banking license so that they would have access to affordable funding in local currency to on-lend. Affinity Africa is one of those digital SME banks that have gone this long and painful route. But in the end, patience pays and in finance one should not cut corners.

Fintech lenders were the disrupters of the last years but it may well be that these disrupters will themselves now be disrupted by banks that succeed in integrating fintech processes and credit assessment methodologies in their existing SME lending businesses.

Closing the SME financing gap: there's still a long way to go

The cycle of success for technology-based SME lenders, both banks and fintech companies, may be slower than wished for. USD 300 billion is a huge gap to close. Lenders need more SME track-records in order to be able to feed a data-pool. Better data will lead to more precise credit scoring. Digitalising data-based processes will cut operational cost, leading to better and more predictable returns which, in turn, should lead to more equity and debt funding for such lenders, which, consequently, would power the expansion of SME lending, leading, then again, to more and better data. More predictable returns lead to more competition and reduced interest rates which should lead many more SMEs to borrow to grow their businesses.

This cycle of success is applicable to both fintech lenders and banks. It is unlikely that this cycle will be fast and that the financing gap for SMEs will be closed in the immediate future. But SME lending will become more profitable and sustainable. Profitable businesses attract funding and this should have a positive impact on the economy in Africa.

____________________________________________________________________________________________________________

About the author

Marcus Fedder is Vice Chair of TCX and an advisor to Affinity Africa. He co-founded a microfinance investment vehicle and prior to that was Vice Chair and Head of Europe and Asia-Pacific for TD Securities, the Toronto Dominion Bank, and Treasurer of the EBRD. He researched SME lending in Africa during a fellowship at the Stellenbosch Institute for Advanced Study (STIAS) in the South African autumn of 2022. His findings were published by the African Development Finance Journal Vol 5 No 4, 2023, pp 154, and provided the basis for this blog.

Your comment