Access to credit for SMEs in North Africa: does family ownership matter?

Sep 26, 2023

Small and medium-sized enterprises (SMEs) account for around half of formal employment in North Africa. These figures would even be significantly higher if SMEs operating in the informal sector were taken into account. Due to a capital market that is largely inaccessible to them, their main source of formal financing remains the banking sector and microfinance. However, the region's SMEs receive only 7% of the credit granted by banks, most of which is channeled to the largest corporations. Of these North African SMEs, around 80% are family businesses. They are very much rooted in the region's culture, and the aim is to pass on the business to the next generation.

Family firms in north Africa: a game changer in gender inclusion

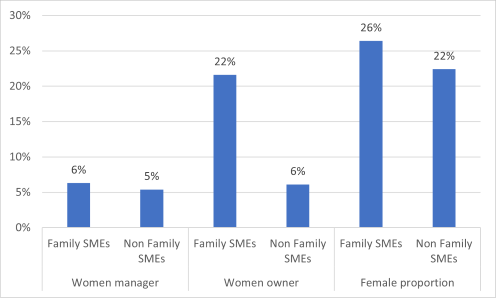

Besides that, some studies have shown that family businesses tend to have more female managers than non-family businesses. Therefore, improving access to finance for family-owned SMEs would be crucial for the region and could also facilitate women’s access to management positions in North Africa, as gender inclusion in business in the region is one of the lowest[1]. Figure 1 shows that there are more female owners and managers of family-owned SMEs than non-family SMEs. Even if the difference is only 1% for the latter, for the former, the gap is 16% in favor of family firms. This is because parents can more easily pass on the business to their children, even when they are women. This is also reflected in the higher proportion of women working in family-run SMEs.

Figure 1: SMEs in North Africa: Gender Participation

Source: World Bank Enterprise Survey (Morocco 2019, Egypt 2020, Tunisia 2020 pooled)

Family ownership: an advantage or disadvantage in access to finance in North Africa

The long-term commitment, and the less risky attitude but also the resilience of family businesses[2] can be advantage in access to credit. In fact, the ability of family firms to pursue business development objectives can make them less risky in the eyes of financing institutions. Moreover, better access to the finance of family firms can also be due to the soft information that the lenders have through personal relationships with the owners. Family businesses strongly value long-term relationships with banking partners.

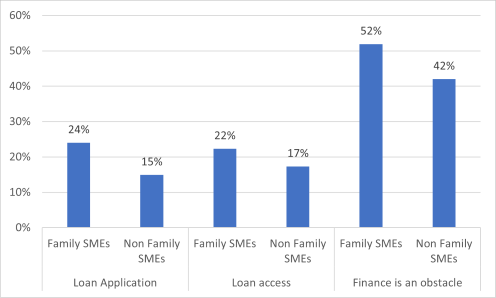

Figure 2: SMEs access to finance in North Africa

Source: World Bank Enterprise Survey (Morocco 2019, Egypt 2020, Tunisia 2020 pooled)

In North Africa, family firms applied more to credit and then have more access to credit (Figure 2). However, while the gap in loan application is 9 percentage points meaning a greater demand from family SMEs, the gap in access to credit is only 5 percentage points. This could point to a greater difficulty in accessing credit for family businesses compared to non-family businesses. Moreover, this is confirmed by the fact that 52% of family businesses see access to financial services as an obstacle to their activities, compared with 42% of non-family businesses. There is evidence that the risk of significant family intervention in business management can have a negative effect on the way banks and other financial institutions perceive them.

A more formal business and monitoring strategy: a solution to improve access to credit for family businesses

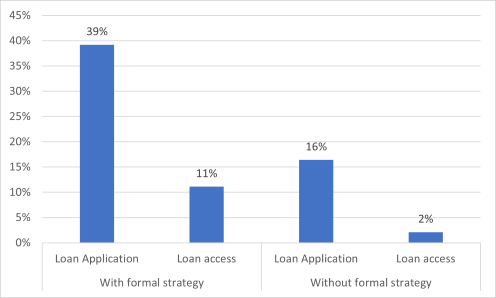

Figure 3: Family firms access to finance: With and without formal business strategy

Source: World Bank Enterprise Survey (Morocco 2019, Egypt 2020, Tunisia 2020 pooled)

Implementing a more formal business strategy can be a solution to the lack of trust in family businesses. A business with well-defined and monitored Key Performance Indicators (KPIs) will help reduce financial inconsistencies and opacity. In North Africa, 39% of family businesses with a well-defined formal strategy apply for loans, compared with only 11% of those without such a strategy (Figure 3). Of course, this is reflected in access to credit: only 2% of family businesses without a formal strategy have access to credit, compared with 16% of those with one. A formal business strategy can therefore influence a company's objectives and operations, in particular its financial planning[3] and therefore its access to finance. The resulting quality and transparency of financial information encourage companies to apply for more loans, considerably increasing their chances of obtaining a loan from the lender.

Measures to formalize business strategy procedures will increase both demand and access to credit among family firms in North Africa. Subsequently, given their size and high proportion among, this will improve access to credit in the region. In addition, as mentioned above, it will ensure that women entrepreneurs do not exclude themselves from the credit market, since these family firms are places where they can flourish more easily. Family businesses are therefore decisive and must be considered to improve the dynamics of the credit market in North Africa.

[1] https://www.ilo.org/wcmsp5/groups/public/---arabstates/---ro-beirut/documents/publication/wcms_446101.pdf

[2] Anderson et al., 2003; Bertrand and Schoar, 2006; D’Aurizio et al., 2015…

About the author

Grakolet Arnold Gourène is the Research Officer at MFW4A. He has experience in development finance, including financial market analysis and household and corporate finance. He also has a strong background in policy analysis and evidence-based research. Prior to joining MFW4A, he worked with the United Nations Economic Commission for Africa (UNECA) in Morocco. At UNECA, he assisted the Commission in formulating policies on access to finance for family businesses and sustainable finance in North Africa. Grakolet was also an Assistant Professor at the Université Jean Lorougnon Guédé in Daloa, Côte d'Ivoire, where he taught courses in applied econometrics. Grakolet earned a PhD in economics and finance from Cheikh Anta Diop University in Dakar, Senegal, where his research focused on the integration of African financial markets into global finance.

Your comment